Will Falling Interest Rates Save APAC Real Assets?

April 2024

We share our views on the evolving global interest rates landscape, the knock-on effects for Asia Pacific (APAC) Real Assets markets, and how 2025 is setting up to be a vintage year for investors across different investment strategies.

KEY HIGHLIGHTS

- Steady Now, Declining Soon: Having peaked, global benchmark interest rates are expected to remain sticky, before tapering marginally throughout 2H 2024. Rates are then projected to stabilise thereafter, before gradually declining through the latter half of 2025 and into 2026.

- Emerging Investment Prospects: The ongoing yield decompression and peak capitalisation (cap) rates in the real assets markets are expected to persist into 1H 2025. This phase, marked by repricing and accompanying refinancing pressures, is poised to unveil compelling options for discerning investors.

- 2025 – A Promising Vintage for Investments: Asset revaluation will be followed by a cyclical reversal that promises unparallelled opportunities to buy assets at cyclically high yields. The confluence of the anticipated market recovery and marginal cap rate compression is primed to catalyse capital returns that have been elusive in recent years, promising attractive total returns over the medium term.

With the first quarter of 2024 wrapped up, the macroeconomic backdrop for APAC real assets remains volatile, as markets continue navigating multiple crosscurrents of geopolitical disputes, inflationary pressures, and shifting demographic dynamics. Nonetheless, while the likely trajectory of interest rate movements will always be opaque, the broad consensus remains for now in favour of a soft landing across the global economy.

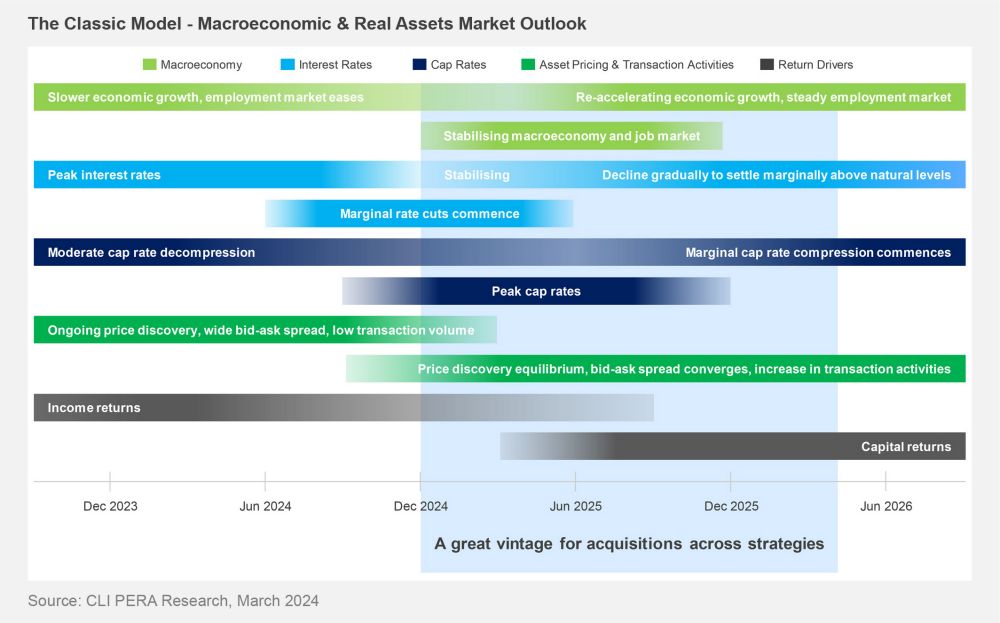

How this applies to APAC as a whole, however, varies from economy to economy. Applying a classic analytical model (see figure below) to major developed markets like Australia and Singapore provides a reasonably comprehensive overview of likely outcomes, in particular an environment of declining interest rates will lead to a rebound in capital returns in the absence of unforeseen externalities such as a recession.

Otherwise, the wide diversity of economic constituencies across APAC has led many individual markets to evolve along distinct tangents that undermine the application of the classic analytical model. Japan, for example, remains an economic outlier for several reasons. Despite the imposition of a long period of low (or even negative) interest rates, external factors can significantly erode capital returns. Such factors include large volumes of cross-border capital flows drawn by Japan’s reputation as a safe haven market, as well as the current global interest rate climate, notably in the form of the positive-carry effect.

A STICKY SITUATION - THE RATE RACE

Incessant pricing pressures experienced by major economies in 2022 convinced most central banks to commence a series of sharp interest rate hikes to combat global inflation. Rate rises tapered and then moved mostly sideways with idiosyncratic volatility for the rest of 2023. Throughout this process, markets remained steadfastly – yet incorrectly – hopeful that the Federal Reserve (Fed) had reached the end of its rate-hiking cycle. However, most benchmark rates have now peaked, and we expect them to remain sticky before again tapering throughout 2H 2024, before stabilising thereafter, and then declining gradually in 2H 2025 through to 2026.

While this bodes well for economic growth generally, declining benchmark rates generally do not imply that banks will be inclined to make corresponding reductions in their own lending rates, especially in relation to commercial real estate borrowing.

As the odds of a global soft landing continue to improve, the timing of upcoming rate cuts has recently been called into question – a result, among other things, of persistently strong headline macroeconomic figures. It is evident that Wall Street strategists have disparate views, and the only real clarity is that even market makers have no coherent model of future outcomes1. Notwithstanding this, it now seems plausible that as inflation steadily cools, the velocity of future rate cuts is likely to be more restrained over the near term.

APAC's ALLURE: BEAUTY IN COMPLEXITY

Anchored by robust demand drivers and solid underlying fundamentals, the region presents pockets of opportunities where investors can adopt highly calibrated investment strategies. By extension, monetary policies across the region are equally diverse. Mirroring the unique economic terrain, they can be broadly characterised into three realms: China, Japan, and rest of the region.

In contrast to the monetary environments in the United States (US) and Europe, APAC’s highly differentiated policy backdrop significantly influences its real assets markets, offering global investors compelling opportunities to achieve attractive risk-adjusted returns, primarily through strategic diversification.

WHAT'S YIELDING NOW?

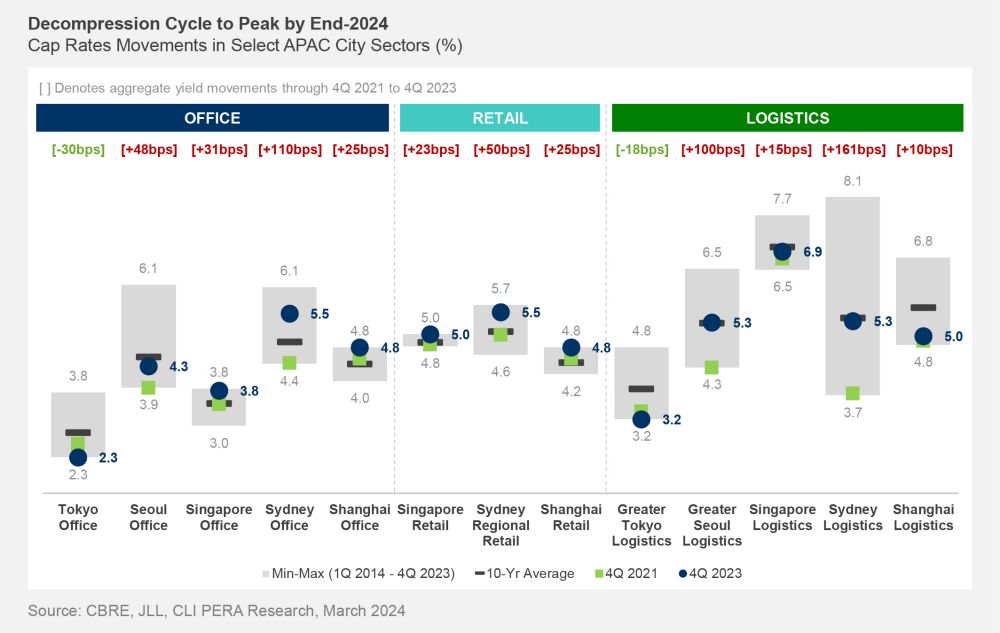

The APAC yield-decompression cycle commenced in early 2022 in tandem with the initiation of global rate hikes, and accelerated for most of 2023, with significant variances across markets (see figure below). The pronounced surge in interest rates has precipitated a substantial increase in borrowing costs and cap rates, driving bid-ask spreads to polarised ends. Consequently, this has notably dampened transaction activities across the region2.

Upward pressure on yields appears to have dissipated in recent months, largely attributed to the tapering of restrictive monetary policies by several central banks in the region. With most markets still adapting to higher borrowing costs and bond yields, we hold the view that the current decompression cycle is likely to persist into late 2024. Yields are projected to stabilise at that point, setting the stage for a period of marginal yield compression from mid- to late-2025, and possibly thereafter.

That said, we are optimistic that bid-ask spreads will begin to narrow as the price discovery phase progresses throughout 2H 2024 and into 1H 2025, setting the stage for transactions to rebound from newly-established (i.e. lower) price points. Looking further ahead, 2H 2025 and 2026 should bring a more pronounced uptick in activities, together with a resumption of capital flows as investors gradually adapt to new-normal underwriting criteria.

As a result, we expect the combination of asset repricing and associated refinancing pressure in some markets to serve as a catalyst for the emergence of compelling buying opportunities. Specifically, high-quality APAC commercial real assets are expected to be the main focus of interest, spurred by an ongoing bifurcation in asset performance compared to lower-quality properties.

2025: A GREAT VINTAGE

Apart from the expected resolution to the bid-ask spread conundrum, we anticipate the uptrend in the post-2024 cycle to be characterised by a number of themes. First, a potentially apparent differentiation should emerge in sector performance, driven by a flight-to-quality mindset and strengthening investor interest in long-term secular themes.

Second, in terms of individual asset classes, we have a strong conviction on the living sector, which we expect to deliver steady returns due especially to evolving regional demographic factors. In addition, modern logistics assets throughout the APAC region will continue to benefit from both sustained occupier demand and the transformative effects of automation, while currently out-of-favour office and retail assets are likely to see a cyclical recovery, albeit with diverging performances across asset grades.

Beyond that, the relentless pace of digitisation and exponential growth in data demand should continue to support the rapid evolution of the data centre sector. Finally, the recent prioritisation of environmental issues, and in particular carbon efficacy, will continue to gain traction as investors come round to the paramount importance of future-proofing investment strategies in order to mitigate heightened risk to asset values.

We remain confident that APAC real assets are strategically positioned for investors to capitalise on the region’s potential for growth within a highly diversified context, not only between individual markets across the region, but also as an entity relative to the US and Europe, with each major country exhibiting its own unique characteristics and market fundamentals.

Above all, the vast array of real assets available across APAC markets offers investors endless possibilities to calibrate and construct efficient, optimal portfolios that align with their respective investment objectives across the risk-return spectrum. With both macroeconomic trends and real assets dynamics suggesting that the conditions are now converging favourably, 2025 is shaping to be a vintage year for investments.

NOTES

------------

1. Market projections for the timing of the Fed’s first rate cut in 2024 are diverse, but generally suggest action sometime between April and September within a range of 25 – 150bps, and most likely between 50 – 125bps. Source: Bloomberg Consensus, CLI PERA Research, as of 31 March 2024.

2. The bid-ask spread conundrum: In a buyer’s market, investors borrow at the current cost of debt, while sellers may already have fixed cost of debt at lower levels. Many sellers are therefore motivated to wait and see if assets eventually revert to lower book values. APAC’s total commercial transaction volume declined 28% YoY to US$140 billion in 2023, significantly lower on a year-on-year basis for the second consecutive year. Source: MSCI Real Capital Analytics, March 2024.

Download the full research paper on CapitaLand Investment's house view on interest rate movements, how 2025 is set to be a vintage year for investments and how to capitalise on opportunities in Asia Pacific.