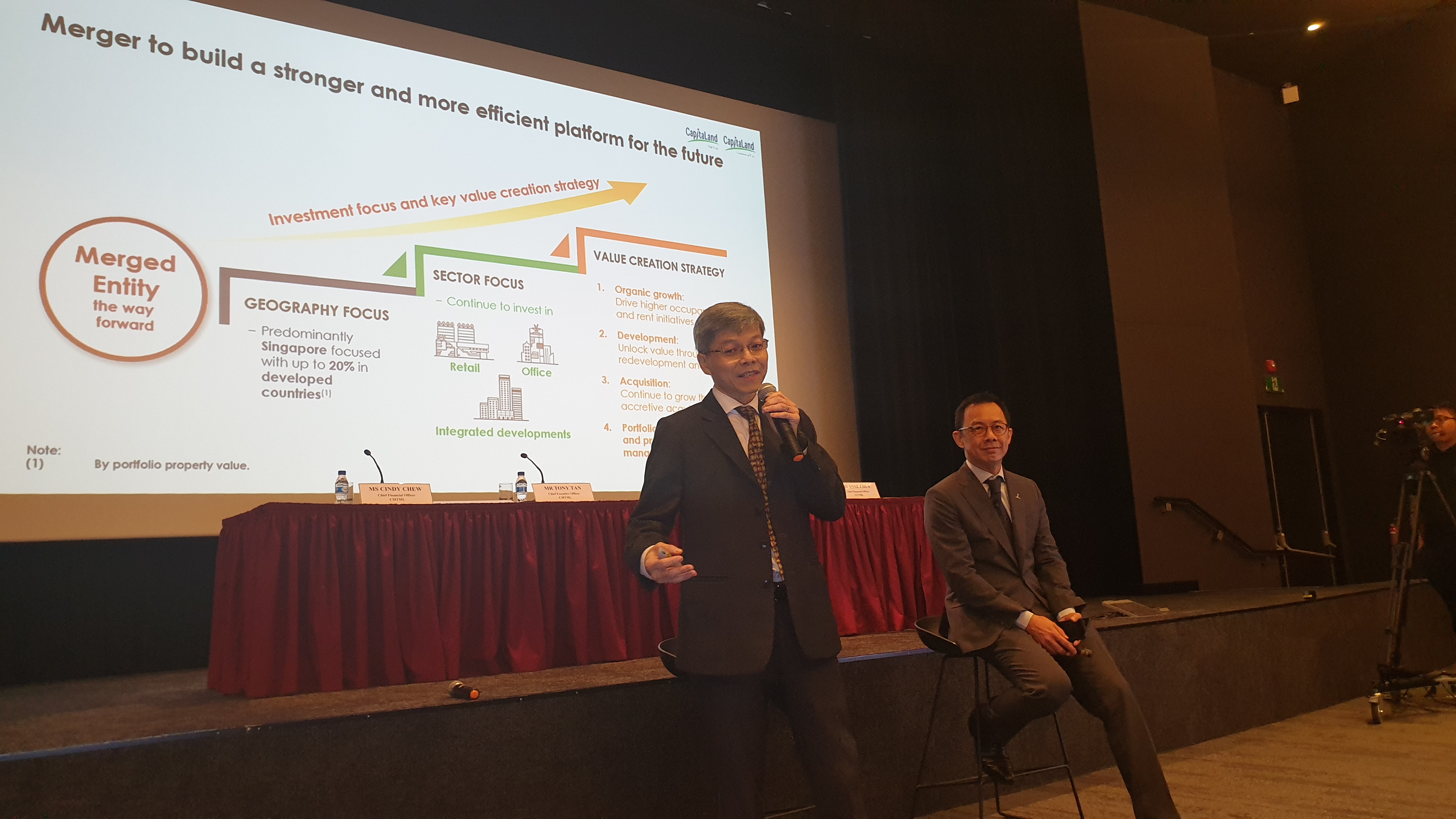

CMT and CCT announce proposed merger to form CapitaLand Integrated Commercial Trust, 3rd largest REIT in APAC

DPU accretive transaction will create the largest proxy for Singapore commercial real estate with a combined property value of S$22.9 billion

22 Jan 2020

Share