Ascendas Reit to acquire 11 last mile logistics properties in Kansas City, United States, for S$207.8 million

22 Oct 2021

Share

CapitaLand Group

With a solid business ecosystem, we deliver long-term sustainable value to our stakeholders.

Global

English

CapitaLand Group

With a solid business ecosystem, we deliver long-term sustainable value to our stakeholders.

22 Oct 2021

Share

Ascendas Reit is acquiring a portfolio of 11 logistics properties located in Kansas City, United States for S$207.8 million.

Singapore, 22 October 2021 – Ascendas Funds Management (S) Limited (the Manager), in its capacity as the manager of Ascendas Real Estate Investment Trust (Ascendas Reit), is pleased to announce the proposed acquisition of a portfolio of 11 logistics properties located in Kansas City, United States (US) (the Target Portfolio or Target Properties), for S$207.8 million (US$156.0 million1) (the Total Purchase Consideration) (the Proposed Acquisition) from ColFin 2017-11 Industrial Owner, LLC and ColFin Cobalt I-II Owner, LLC, third party vendors (collectively, the Vendor).

Mr William Tay, Executive Director and Chief Executive Officer of the Manager said, “This acquisition of 11 logistics properties in Kansas City marks our first entry into the US logistics market and is complementary to Ascendas Reit’s existing logistics portfolio.

The strong market fundamentals driven by rising warehousing requirements for e-commerce fulfilment has led to record net absorption levels and rent growth across the country. We are confident of the growth potential of this portfolio given Kansas City’s geographically central location within the US and its well-developed transportation infrastructure. We believe that there will be continuous high demand for this portfolio, which comprises 200,000 sqm of last mile logistics space offering convenient access to the domestic market, midwestern population centres and other commercial hubs across the country.”

William Tay, Executive Director and CEO of Ascendas Reit's manager

Key Merits of the Proposed Acquisition

1. Kansas City’s logistics sector is well-supported by its skilled workforce and geographically central location

Kansas City’s logistics sector benefits from a growing population as well as a highly skilled workforce. Its population has increased by almost 21% since 20002. More than 37.7% of its residents above age 25 have a bachelor’s degree or higher, compared to the US average of 33.1% and about 5.9% of its workforce are employed in the transportation and warehouse industry, higher than the 4.75% nationally. The city’s unemployment rate of 3.8% (as at August 2021) is also lower than the US average of 5.2%3.

Kansas City’s economy is supported by a wide variety of businesses and key industries include transportation and distribution, eCommerce, manufacturing, animal health, technology and the financial industry.

Its central location between key cities such as Chicago, St. Louis, Dallas and Denver, coupled with its excellent ground, rail and air transportation network, makes Kansas City an ideal Midwestern region logistics hub. From Kansas City, 85% of the nation’s population can be reached within two days4.

Located at the crossroads of the nation’s major interstate highways such as I-35, I-70, and I-29, Kansas City has 30% more interstate miles per capita than any other city in the US. It is also the largest rail centre in the US (in tonnage terms) and has five Class 1 rail lines intersecting the region, four of which have intermodal facilities5.

The Kansas City International Airport is one of the best locations in the US for air cargo and distribution development, moving more air cargo than any other airport in the six-state region. A new US$1.5 billion airport terminal is expected to complete in 20226.

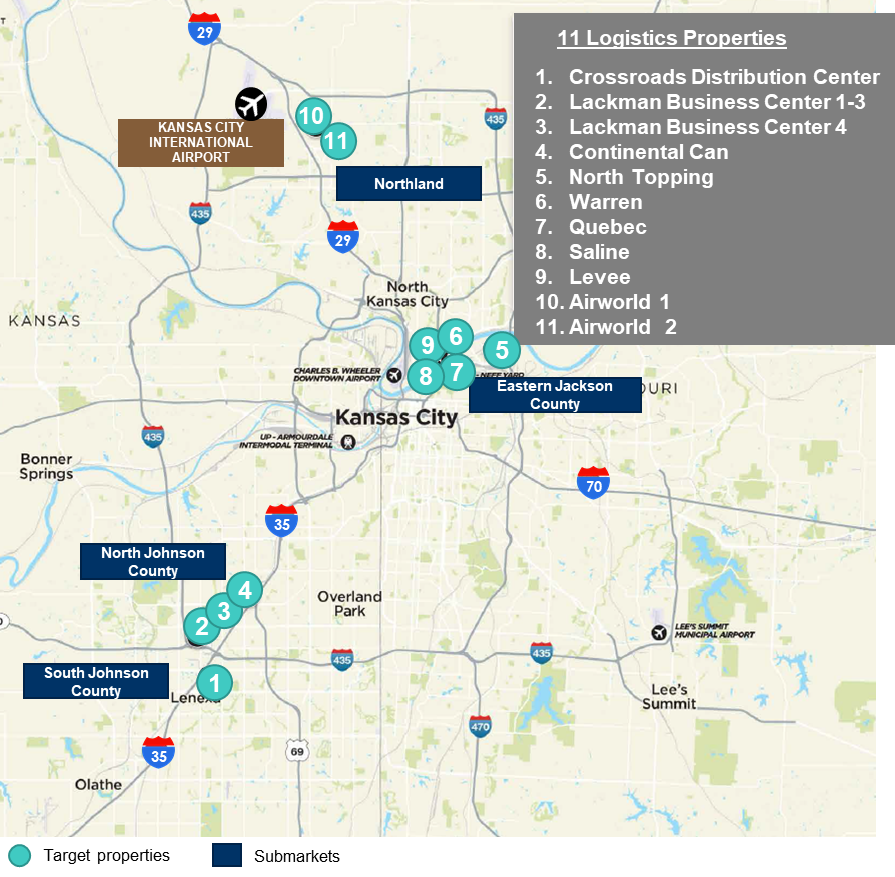

2. Target Properties are located in established submarkets with last mile locations

The Target Properties are located in infill locations across the established submarkets of South Johnson County, North Johnson County, Eastern Jackson County and Northland. These four submarkets house approximately 70% of the overall inventory in the Kansas City market7.

With close proximity to the interstate highways and high density population areas, these submarket locations provide logistics tenants good access to a broad base of customers and employees. For example, the properties in South and North Johnson Counties are located close to the growing and affluent suburbs to the south and west of the city, properties in Eastern Jackson County have direct access into the urban core including downtown Kansas City, and the Northland submarket is well connected to three key interstate highways (I-35, I-29 and I-435) and the Kansas City International Airport, allowing tenants to serve the local economy as well as the greater region.

3. Strong logistics market fundamentals8

Kansas City is ranked 17th in the US based on logistics market size (approximately 27.9 million sqm).

Demand for logistics space in Kansas City has been strong. The overall vacancy rate of the sector has remained low and stable at between 4.5% and 5.9% since 2015. As at 3Q 2021, the vacancy rate for the logistics sector was 4.8%.

In 2020, Kansas City’s net absorption of 548,000 sqm ranked it 8th amongst the US markets. Over the last 5 years (2016 to 2020), average annual net absorption was approximately 520,000 sqm and the average asking rent (triple-net basis) has grown by approximately 3.8% per annum, demonstrating the city’s strong logistics market fundamentals.

E-commerce, third-party logistics, food and beverage and automotive manufacturing users have been the primary demand drivers for logistics space in Kansas City.

4. Attractive property and portfolio characteristics

The 11 properties are located on freehold land and have highly functional designs. The properties have sizes that range between 6,800 sqm and 32,337 sqm which are well-suited for the typical mid-size space demand in the infill locations.

The highly attractive locations of the Target Portfolio contribute to its strong retention rate. Current tenants have been in place for an average of 12.5 years.

5. Stable and diversified income stream

The Target Portfolio is 92.6% occupied by 27 customers from diverse industries such as third-party logistics, wholesale distribution, manufacturing and healthcare. No single customer contributes to more than 10% of the total rental income as at 30 September 2021 of the Target Portfolio, thus minimising tenant concentration risk. The current leases also have built in annual rental escalations ranging between 2.5% and 3.0%.

6. Diversifies Ascendas Reit’s logistics exposure

The Proposed Acquisition is expected to increase and diversify Ascendas Reit’s exposure to logistics properties. On a pro forma basis, the Proposed Acquisition will increase the proportion of logistics properties to 22% (S$3.5 billion) of total investment properties of S$16.2 billion (from 21% or S$3.3 billion as at 30 September 2021).

The logistics portfolio will also be spread across the four developed markets of Australia (S$1.3 billion), Singapore (S$1.2 billion), United Kingdom (S$0.8 billion) and the US (S$0.2 billion) compared to three markets prior to the Proposed Acquisition.

7. Distribution per Unit (DPU) accretive acquisition

The estimated net property income (NPI) yield9 for the first year post acquisition is approximately 5.1% and 5.0% pre-transaction costs and post-transaction costs respectively.

The Manager intends to redeploy the proceeds from its recent divestments of three logistics properties in Australia10 to partially finance the Proposed Acquisition. The remaining balance will be financed through existing debt facilities. Based on this funding structure, the pro forma impact on the DPU for the financial year commencing on 1 January 2020 and ended 31 December 2020 is expected to be an improvement of 0.11 Singapore cents or a DPU accretion of 0.73% assuming the Proposed Acquisition was completed on 1 January 202011.

The portfolio comprises 200,000 sqm of last mile logistics space offering convenient access to the domestic market, midwestern population centres and other commercial hubs across the country.

Valuation of Target Portfolio

In connection with the Proposed Acquisition, an independent valuation on the Target Portfolio was commissioned by HSBC Institutional Trust Services (Singapore) Limited (in its capacity as trustee of Ascendas Reit)[1]. The independent valuation concluded an aggregate market value of US$156.3 million for the Target Portfolio as of 24 September 202113.

Transaction Costs

Ascendas Reit, through its indirect wholly owned subsidiary, Ascendas Reit US 1 LLC, entered into a purchase and sale agreement with the Vendor to acquire the Target Portfolio.

The Total Purchase Consideration of S$207.8 million (US$156.0 million) was negotiated on a willing-buyer and willing-seller basis.

The completion of the Proposed Acquisition is subject to closing conditions and is expected to take place in 4Q 2021. On completion, the Total Purchase Consideration (less the deposit which has been previously paid to the Vendor) will be payable to the Vendor in cash.

Ascendas Reit is expected to incur an estimated transaction cost of S$4.4 million (US$3.3 million), which includes stamp duty, professional advisory fees, and acquisition fees payable to the Manager in cash (being 1% of the Total Purchase Consideration which amounts to approximately S$2.08 million (US$1.56 million)).

Ascendas Reit will, upon completion of the Proposed Acquisition, own 221 properties. Its total investment properties is expected to be worth approximately S$16.2 billion14 comprising 97 properties (S$10.0 billion15) in Singapore, 41 properties in the US (S$2.3 billion), 34 properties (S$2.1 billion) in Australia and 49 properties (S$1.8 billion) in the UK/Europe.

Please refer to the Annex for more details.

The logistics properties are located in infill locations across the established submarkets of South Johnson County, North Johnson County, Eastern Jackson County and Northland. These four submarkets house approximately 70% of the overall inventory in the Kansas City market.

Notes:

1 An illustrative exchange rate of US$1.000: S$1.332 is used for all conversions from US Dollar into Singapore Dollar amounts in this press release.

2 Source: CBRE, 2021, Why Kansas City

3 Source: U.S. Bureau of Labor Statistics

4 Source: CBRE Research, 2020 North America Industrial Big Box, Review & Outlook

5 Source: CBRE, 2021, Why Kansas City

6 Source: CBRE Research, 2020 North America Industrial Big Box, Review & Outlook

7 Source: Newmark Zimmer, Q3 2021 Kansas City Industrial Market report

8 Source: Newmark Zimmer data, Q4 2020 and Q3 2021, Kansas City Industrial Market reports

9 The NPI yield is derived using the estimated NPI in the first year after acquisition.

10 See announcement dated 9 July 2021 “Completion of divestment of three logistics properties in Australia”.

11 The pro forma DPU impact is calculated based on the following assumptions a) Ascendas Reit had completed the Proposed Acquisition on 1 January 2020, held and operated the Target Properties through 31 December 2020, b) the Proposed Acquisition was funded using proceeds from its recent divestments in Australia and existing debt facilities, and c) the Manager elects to receive its base fee 80% in cash and 20% in units. Assuming the Proposed Acquisition was funded based on a funding structure of 40% debt and 60% equity, the pro forma DPU impact is expected to be an improvement of 0.006 Singapore cents.

12 This is in accordance with the requirements of Appendix 6 of the Code on Collective Investment Schemes issued by the Monetary Authority of Singapore.

13 The independent valuer, CBRE Valuation & Advisory Services, has valued the Target Portfolio based on the sales comparison and discounted cash flow approaches.

14 As at 30 September 2021, excluding three properties in Singapore under redevelopment.

15 Asset value excludes three properties in Singapore under redevelopment.

A. Summary of Proposed Acqusition

Total Purchase Consideration |

S$207.8 m (US$156.0 m) |

Acquisition Fee, Stamp Duty and Other Transaction Costs |

S$4.4 m (US$3.3 m) |

Total Acquisition Cost |

S$212.2 m (US$159.3 m) |

B. Locations of Target Properties

The 11 logistics properties are located on freehold land across Kansas City’s submarkets of South Johnson County, North Johnson County, Eastern Jackson County and Northland.

C. Summary of Target Portfolio (as at 30 September 2021)

Number of Properties & Asset Type |

11 logistics properties |

Land Area |

432,241 sqm |

Land Tenure |

Freehold |

Total Net Lettable Area (NLA) |

200,908 sqm |

Weighted Average Lease Expiry (by rental income) |

2.8 years |

Occupancy Rate |

92.6% |

Total Number of Unique Customers |

27 |

Lease Structure |

Majority triple-net |

D. Details of Target Properties (as at 30 September 2021)

|

Property name |

Address |

Land Area (Sqm) |

NLA (Sqm) |

Occupancy |

1 |

Crossroads Distribution Center |

11350 Strang Line Road |

40,913 |

16,259 |

100% |

2 |

Lackman Business Center 1-3 |

15300 – 15610 West 101st Terrace |

88,868 |

32,337 |

100% |

3 |

Lackman Business Center 4 |

15555 – 15607 West 100th Terrace |

17,199 |

6,800 |

100% |

4 |

Continental Can |

11725 West 85th Street |

31,161 |

15,946 |

100% |

5 |

North Topping |

1501 – 1599 North Topping Ave |

23,552 |

11,066 |

100% |

6 |

Warren |

1902 – 1930 Warren Street |

45,729 |

23,826 |

100% |

7 |

Quebec |

1253 – 1333 Quebec St |

41,359 |

28,935 |

49% |

8 |

Saline |

1234 – 1250 Saline St |

21,489 |

11,073 |

100% |

8 |

Levee |

1746 Levee Rd |

54,227 |

22,125 |

100% |

10 |

Airworld 1 |

10707 – 10715 Airworld Drive |

38,971 |

18,580 |

100% |

11 |

Airworld 2 |

10717 Airworld Drive |

28,773 |

13,961 |

100% |

|

Total |

|

432,241 |

200,908 |

92.6% |

For media queries, please contact us at:

media@capitaland.com

Share