Insights from CLI: Tracking AI's Impact on Offices and Business Parks in APAC

09 Apr 2026

Share

CapitaLand Group

With a solid business ecosystem, we deliver long-term sustainable value to our stakeholders.

Global

English

CapitaLand Group

With a solid business ecosystem, we deliver long-term sustainable value to our stakeholders.

CapitaLand Group

With a solid business ecosystem, we deliver long-term sustainable value to our stakeholders.

09 Apr 2026

Share

Artificial intelligence (AI) will be one of the most consequential technological shifts of the current era. It will fundamentally rewire firms’ decision around business processes, organisation structure, talent strategies, and physical footprints. Understanding this structural and broad-based shift is essential context for assessing the long-term trajectory of occupier demand for office and business park (BP) sectors.

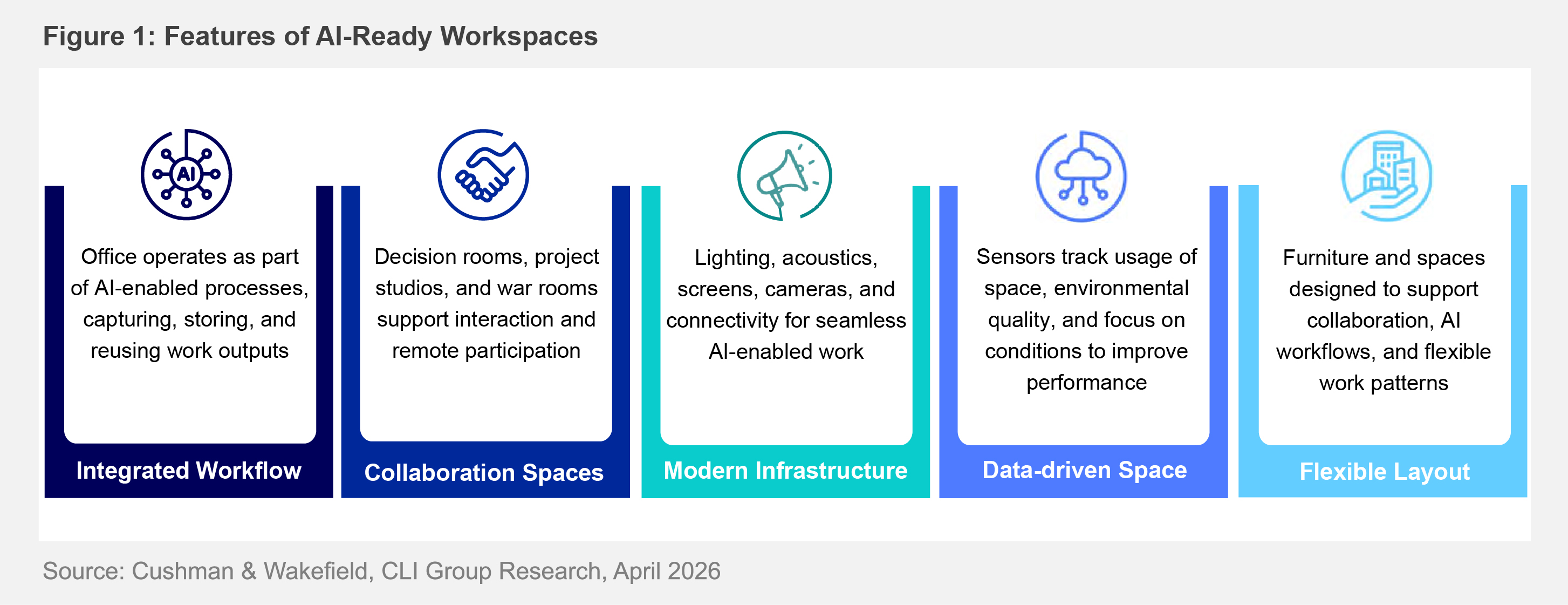

What kinds of workspaces remain essential in an AI-enabled economy? Based on CapitaLand Investment (CLI)’s engagement with occupiers across Singapore, China and India, the emerging pattern is not a broad-based contraction, but a redistribution of demand. AI is accelerating a K-shaped divergence: high-specification, well-located and infrastructure-ready assets will remain integral to business operations, while commoditised space will face structural pressure. The role of the workplace will shift from a site of routine task execution to a platform for decision-making, innovation and human- AI collaboration (Figure 1). Markets with significant supply pipelines and/or high proportion of commoditised space will face challenges. AI-driven efficiency gains are compressing space needs in back-office and support functions, and some occupiers are actively consolidating footprint as headcount-to-desk ratios tighten.

Across CLI’s portfolio, tenant requirements are increasingly centred on infrastructure readiness, collaboration density and the ability to support data-intensive workflows. These factors feature prominently in both new leasing decisions and renewal negotiations. The flip side is that space which cannot meet these requirements is losing relevance faster than before, as older stock with limited upgrade potential faces occupancy losses and value reduction overtime1.

AI is redistributing jobs, not just eliminating them. While AI-driven job displacement is a widely discussed concern, historical data points to a more complex and ultimately more optimistic outcome.

Though previous technological advances eliminated certain tasks, they also created entirely new categories of work. Roughly 60% of US workers today hold jobs that didn’t exist in 1940, and technology has driven 85% of employment growth since then³. AI represents the latest iteration of this dynamic – it is replacing tasks, not just eliminating them.

While AI is automating routine tasks in many sectors, AI adoption has the potential to generate superior revenue and productivity outcomes, not solely to reduce costs4. Industries most exposed to AI saw three-times higher growth in revenue per employee compared to those least exposed5.

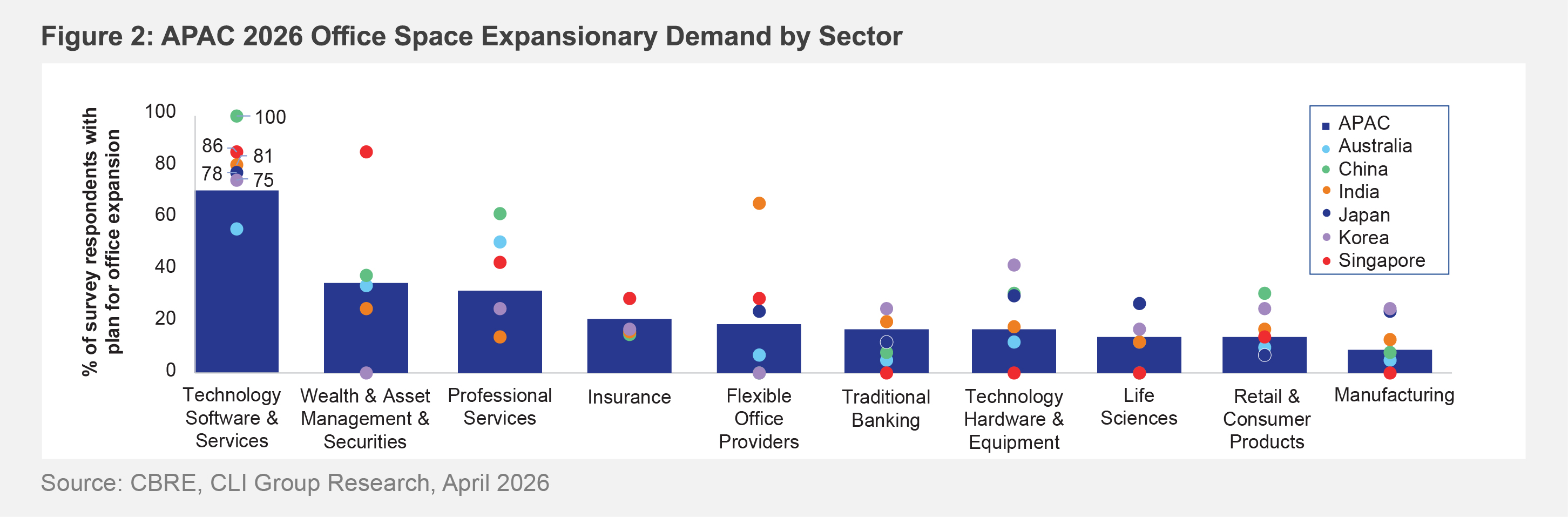

Early adopters of AI are also expanding their workforces, and for specialised, higher-skilled roles that can work alongside and leverage AI capabilities. Across APAC, office employment is projected to grow steadily by 3.5% in 20266. However, office occupiers’ expansion plans vary significantly by country and sector. The technology sector (including Big Data and AI) recorded the highest proportion of occupiers planning to expand, led by China, Singapore, and India. In contrast, fewer than half of tenants in other sectors indicated intentions to expand (Figure 2).

The transition to higher-value roles will not be without challenges, and some frictional unemployment is expected as workers adapt and reskill. The pace and severity of adjustment will be shaped by labour market conditions and government reskilling initiatives. According to World Economic Forum’s four futures for jobs in 20307, employment is likely to face greater volatility and systemic risk when AI advances at a greater pace than the workforce’s ability to adopt. On the other hand, when the workforce is ready to integrate AI development in various workflows, there is potential for further augmentation, with human-AI collaboration to reshape value chains and business models.

AI is unlikely to reduce the relevance of physical workspace across APAC, but it will reshape its purpose and value. Demand will become more selective, concentrating in locations and assets that can support innovation, coordination and still-nascent but increasingly complex human-AI workflows.

For investors, this reinforces a more selective allocation approach. Core capital should prioritise office and business parks with enduring demand visibility, while value-add opportunities could be pursued to unlock relevance through asset repositioning. At the same time, capital should be rotated away from structurally challenged stock, and towards sectors and strategies benefiting from AI-driven demand (e.g. data centres, tech-enabled logistics) and complementary capital structures such as real estate private credit. As dispersion widens, performance will be increasingly driven by asset selection and execution rather than broad market movement.

For more in-depth market analysis on AI's impact on workspaces in Singapore, India and China, get the full report.

Note:

1. Source: JLL – “Futureproofing 4.0: Opportunity through Obsolescence”, April 2025.

2. Source: The Budget Lab – “Evaluating the Impact of AI on the Labour Market: Current State of Affairs”, October 2025.

3. Source: Goldman Sachs – “How Will AI Affect the Global Workforce?”, August 2025.

4. Source: PwC – “Leading Through Uncertainty: AI’s Impact on the Workforce”, March 2026.

5. Source: PwC – “AI Fuels Fourfold Productivity Gains With Job Growth Bucking Expectations: PwC’s 2025 Global AI Jobs Barometer”, 2025.

6. Source: CBRE – “2026 Asia Pacific Real Estate Market Outlook”, January 2026.

7. Source: World Economic Forum – “The Future of Jobs: 6 Decision-Makers on AI and Talent Strategies”, January 2026.