APAC Opportunity Map – Private Real Assets Outlook 2026

04 Feb 2026

Share

CapitaLand Group

With a solid business ecosystem, we deliver long-term sustainable value to our stakeholders.

Global

English

CapitaLand Group

With a solid business ecosystem, we deliver long-term sustainable value to our stakeholders.

CapitaLand Group

With a solid business ecosystem, we deliver long-term sustainable value to our stakeholders.

04 Feb 2026

Share

Executive Summary

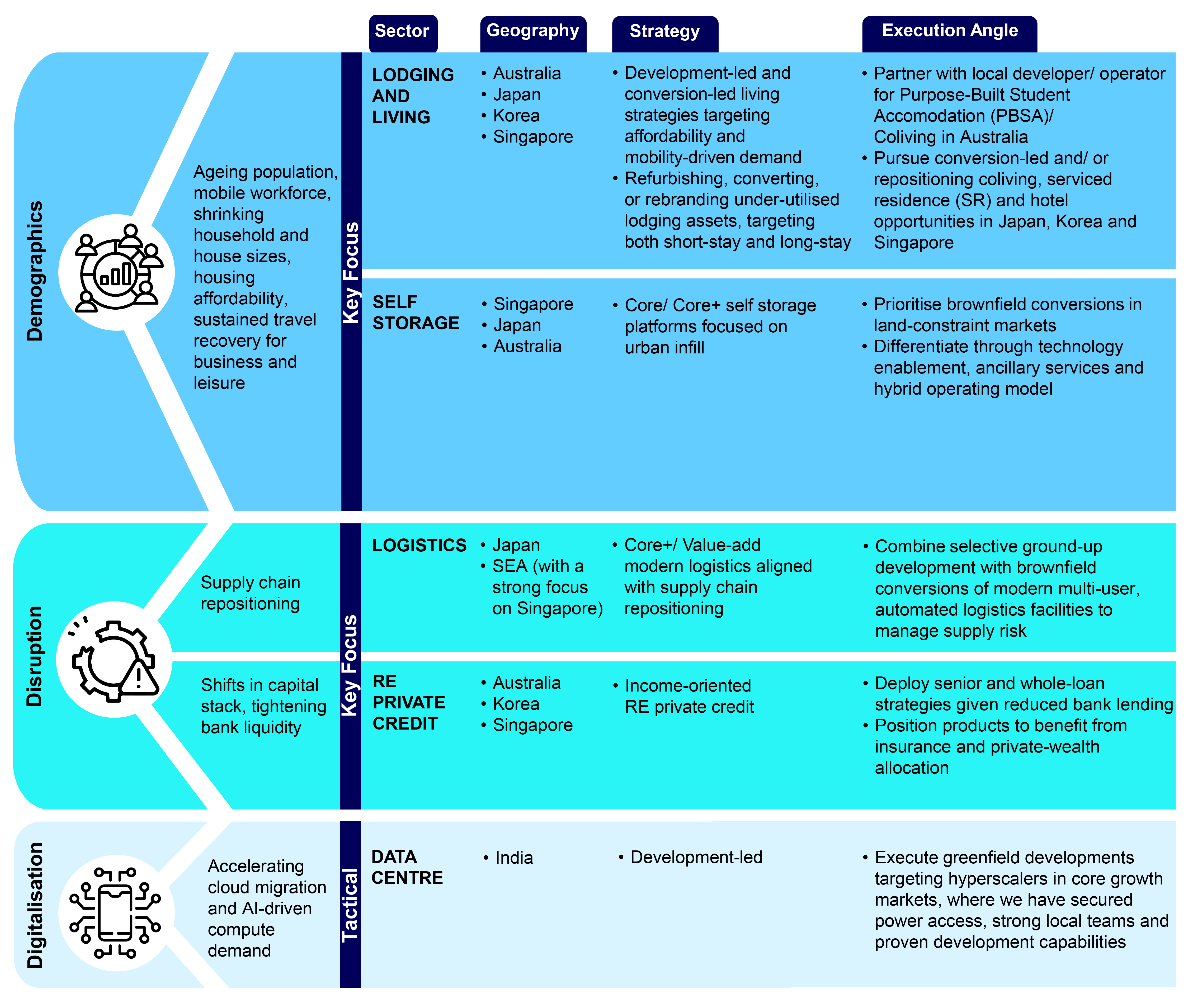

With transaction activity normalising after rate tightening at a faster pace than other regions*, APAC is reasserting itself as a key allocation within global real asset portfolios. The region’s 2026 investment case is structural rather than cyclical – an increasingly important distinction as global growth and policy paths diverge. CapitaLand Investment (CLI) continues to anchor our APAC allocation thesis on Lodging and Living, Self Storage, Logistics, Real Estate (RE) Private Credit, and opportunistically on Data Centre, where durable demand drivers differentiate the region from slower-growing developed markets.

Monetary conditions have moved incrementally in the region’s favour, reducing rate uncertainty and improving underwriting visibility. At the same time, elevated construction costs have constrained development pipelines across many developed APAC markets.

That said, geopolitics, climate impacts, cyber exposure and uneven macro cycles are identified as key increasingly correlated risks. In this environment, portfolio construction must prioritise resilience and optionality over precision forecasting.

We therefore favour a barbell approach to capital deployment:

· Defensive income strategies, including Core/Core+ RE and income-oriented RE private credit, to provide cash-flow visibility and downside protection; and

· Secular growth exposures supported by long-duration demand drivers that are macro-resilient.

Our 2026 base case is for elevated uncertainty without systemic dislocation. Opportunity is more likely to arise from market inefficiencies and capital-structure complexity rather than broad repricing. Platform transactions, recapitalisations, development pauses and bespoke credit solutions will be key investment channels, shaped by diverse regulatory regimes and market dynamics that place a premium on scale and local capabilities.

Against this backdrop, balance-sheet flexibility is becoming a critical differentiator. Asset managers that are able to deploy capital directly through seed investments, warehousing or co-investment structures are better positioned to act on time-sensitive and off-market opportunities, offering investors improved access, greater execution certainty and stronger alignment in complex situations.

Our conviction is that APAC’s next investment cycle will continue to be shaped by three enduring structural forces – Demographics, Disruption and Digitalisation – creating persistent demand across lodging and living, self storage, logistics, asset-backed private credit and data centres. In a market defined by limited supply, rising replacement costs and capital scarcity, these sectors offer the strongest combination of pricing power, downside protection and long-term growth.

Our primary areas of focus are Lodging and Living, Self Storage, Logistics and RE Private Credit. Sustained travel recovery underpins demand for lodging assets while urbanisation, household formation and ageing population are key growth drivers for modern living solutions. E-commerce penetration, supply-chain reconfiguration and inventory localisation are structurally increasing the need for logistics and storage infrastructure. We are prioritising partnerships with local developers, brownfield conversions in land-constrained markets and selective ground-up development to manage delivery risk while capturing structural growth.

In parallel, we are scaling income-oriented RE private credit strategies to benefit from reduced bank lending and increasing institutional demand for asset-backed income. Leveraging digitalisation trends, Data Centre is pursued selectively in high-growth markets where we have long-standing presence, established local teams, reliable power accessibility and a strong development track record.

Note:

*APAC 2025 investment volume was US$ 204 billion (14% below 2021 level), compared to Americas at US$ 477 billion (42% below 2021 level) and EMEA at US$ 224 billion (41% below 2021 level). Source: RCA, January 2026.